1 MIN READ

Activation

The activation gap is the cheapest line on your P&L to fix

Why activation is the easiest lift to your P&L

Daniel West

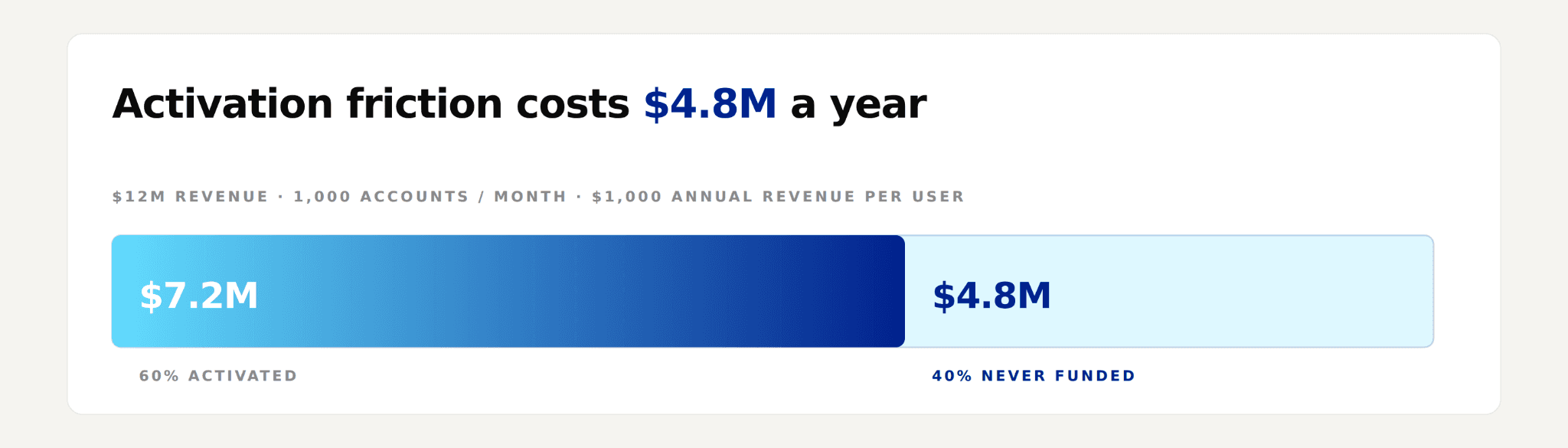

Billions of dollars in revenue walk out the door every year through activation. 60% of business accounts opened never become primary relationships. 40% never get funded at all. The other 20% fund but never move income, payroll, spend, vendors, or clients off the old account. What's left is a name in the system, the cost of acquisition on the books, and a customer who never became one.

The math

A fintech bringing in 1,000 new business accounts a month at $1,000 annual revenue per user generates $12M in annual revenue from that cohort. Lose 40% to never-funded and $4.8M walks out the door every year.

These numbers are conservative. Include the accounts that fund but never operationalize and it compounds. In customer data we've seen, accounts where income moves to the new bank within seven days deliver 95% higher lifetime value than accounts where it doesn't. The longer income takes to move, the worse the retention math gets.

The reverse is also a curve. The longer income takes to move, the worse the retention math gets.

Why this is the cheapest spot to fix

Everything expensive already happened upstream. You already paid to acquire the customer, and they went through the whole process to open the account. The customer chose this account over the next-best alternative while the cost of acquisition sits on the books.

What's left is operationalizing these accounts to avoid lost CAC. Moving income from Stripe, payroll from Gusto, and vendors from Bill.com are all required to deliver top account returns.

Fixing the activation gap is where you ensure acquisition cost doesn’t go to waste.

What banks see in the same data

Curinos reports primary customers hold 10x more deposits than non-primary. That ratio is what makes activation a deposit growth story. At the industry level, 5.4 million businesses attempt a bank switch every year. The failures cost the industry $72B annually.

Where the work lives

We did 300 manual switches before a line of code at InstaSwitch, and it made one thing clear. Switching is a software problem. Income doesn't move because Stripe needs an update. Payroll doesn't move because Gusto needs an update. Spend doesn't move because the corporate card on file in 20 vendor portals needs an update. Each of those is a separate flow with a different process.

The work to fix that is what InstaSwitch handles. Real switching at the portal level across Gusto, Stripe, Square, QuickBooks, Bill.com, Shopify, and 30+ others. Over 35 automations completing common switches in under 30 seconds. Over 350 guided updates for everything else.

If account opening is outpacing activation, the next 90 days of growth are sitting in deposits that never land and accounts that never become primary.The acquisition spend stays the same either way.

If you want to see what the activation gap is costing you specifically, let’s walk through it together with your numbers.

See what the activation gap costs you → Book Time Here